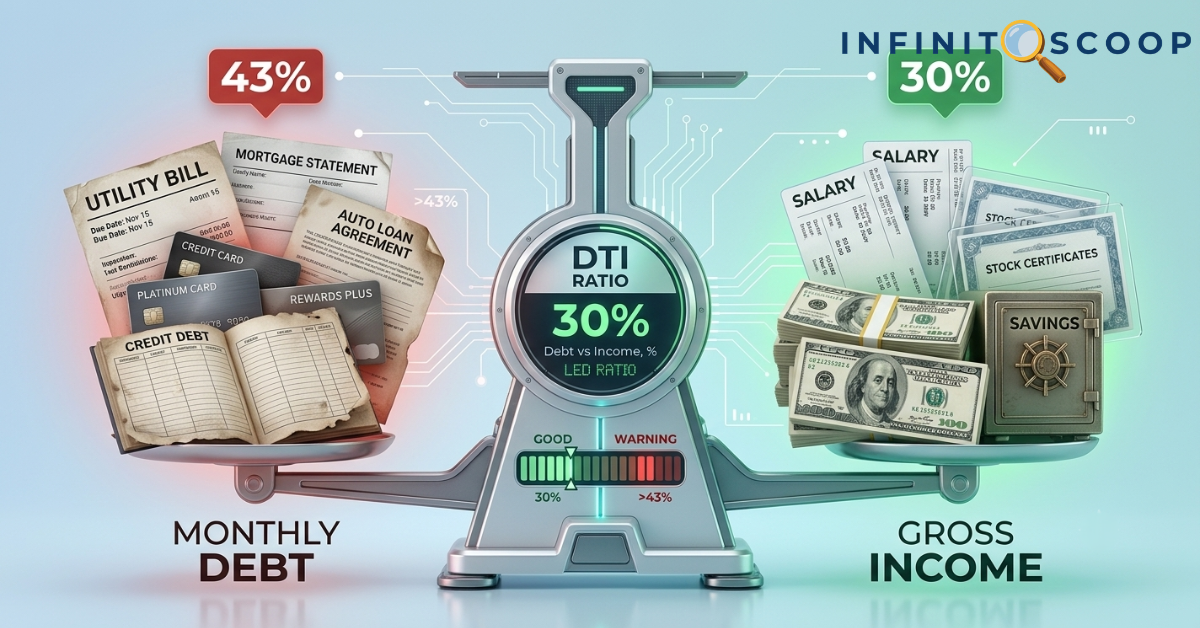

Ever wonder what lenders see when they look at your financial profile? While everyone obsesses over credit scores, smart borrowers know there is another number that quietly pulls all the strings. It is your debt-to-income (DTI) ratio.

Think of your credit score as your financial reputation, while your DTI is your actual breathing room. If you want to secure the best mortgage rates or smooth loan approvals, you need to understand this metric inside out. Let us pull back the curtain on what a good DTI looks like and how you can optimize yours today.

What Is a Debt-to-Income Ratio and How to Calculate It

Your DTI is simply the percentage of your gross monthly income that goes toward paying off recurring debts. It tells a lender exactly how much cash you have left over after meeting your current obligations each month.

The math behind it is incredibly simple. Just use this quick formula:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

To map this out yourself, follow these quick steps:

- Step 1: Add up your monthly debt obligations. Include mortgage or rent payments, auto loans, student loans, personal loans, and minimum credit card payments. Do not include regular living expenses like groceries, utilities, phone bills, or streaming subscriptions.

- Step 2: Divide that total by your gross monthly income. Remember to use your pre-tax income, not your take-home pay.

- Step 3: Multiply the result by 100 to get your final percentage.

For example, if your monthly debts add up to $1,800 and your pre-tax monthly income is $5,500, your DTI sits at 32.7%. This is a strong, highly attractive percentage that tells banks you are a safe bet.

Front-End vs. Back-End DTI: The Big Difference

When you apply for a home loan, underwriters do not just look at one flat percentage. They actually evaluate two distinct types of DTI to get a complete picture of your financial health.

- Front-End DTI (The Housing Ratio): This looks strictly at your future housing costs. It adds up your projected mortgage principal, interest, property taxes, home insurance, and any HOA fees, then divides that by your gross income. Lenders generally love to see this number stay under 28%.

- Back-End DTI (The Total Ratio): This is the heavy hitter. It combines your housing expenses with every other recurring monthly debt you owe. When a financial professional asks about your DTI, they are almost always talking about this specific number. The ideal sweet spot is under 36%, though many programs accept up to 43%.

The Essential DTI Cheat Sheet

| DTI Type | What It Measures | Target Range |

| Front-End | Housing costs only ÷ gross income | Under 28% |

| Back-End | All monthly debts ÷ gross income | Under 36% |

Decoding the Complete DTI Range Breakdown

Where does your percentage land on the spectrum? Understanding these tiers helps you know exactly how much bargaining power you have before stepping into a bank.

| DTI Range | Category | What It Means for You |

| Under 28% | Excellent | Unlocks the lowest interest rates, lightning-fast approvals, and maximum borrowing limits. |

| 28% – 36% | Good | Indicates a very strong profile. You will easily qualify for the most competitive market offers. |

| 36% – 43% | Acceptable | Approvals are still highly likely if you have solid credit, though interest rates might tick slightly higher. |

| 43% – 50% | High | Your financing options start to narrow. You will likely need to look at government-backed loan programs. |

| Above 50% | Too High | Most traditional lenders will issue an automatic decline. You need to focus on debt reduction first. |

Industry data shows that keeping your ratio under 36% consistently secures the lowest interest rates. A low DTI is not just an approval pass; it is a powerful rate-negotiation tool.

DTI Benchmarks by Loan Program

Different loan types operate under different sets of rules. Here is a clear look at the maximum limits allowed across major financing options.

| Loan Type | Max Front-End DTI | Max Back-End DTI | Key Takeaways & Program Notes |

| Conventional | 28% | 36% – 45% | Can stretch up to 50% through automated underwriting if your profile is strong. |

| FHA Loan | 31% | 43% | Highly flexible for lower credit scores; can hit 50% with compensating factors. |

| VA Loan | No strict limit | 41% benchmark | No official maximum cap; underwriters focus heavily on your remaining residual income instead. |

| USDA Loan | 29% | 41% | Designed for rural properties; can go up to 44% with strong financial backup. |

| Personal Loan | N/A | 40% – 45% | Guidelines vary wildly depending on the specific private lender you choose. |

If your ratio is on the higher side, lenders look for “compensating factors” to offset the risk. Having deep cash reserves, an excellent credit score, a massive down payment, or long-term job stability can tip the scales in your favor.

The Synergy Between Credit Scores and DTI

Many people treat their credit score and their debt load as isolated metrics. In reality, they are deeply connected.

| Credit Score | DTI Level | Expected Approval Outcome |

| High Score | Low DTI | Premium rates, effortless underwriting, and maximum loan limits. |

| High Score | High DTI | You might still qualify, but your total loan amount will be restricted and rates will rise. |

| Low Score | Low DTI | Approval takes more work, but your clean debt load heavily offsets your weaker score. |

| Low Score | High DTI | Severe risk of immediate rejection. You must prioritize fixing your numbers before applying. |

Here is a major insider tip: DTI is the fastest financial variable you can change. While building a credit score takes months of flawless history, paying down a credit card balance can drop your DTI and shift your approval odds within a single billing cycle.

Does DTI Directly Impact Your Credit Score?

The short answer is no. Your DTI ratio is not printed on your credit report, and FICO does not use it to calculate your score.

However, the indirect connection is massive. High credit card balances simultaneously inflate your DTI and spike your credit utilization ratio, which dictates 30% of your credit score. Knocking down revolving debt gives you an instant double win: it shrinks your DTI and elevates your credit score at the exact same time.

6 Fast Ways to Shrink Your DTI Ratio

If you want to optimize your numbers quickly before speaking to a loan officer, prioritize these proven strategies.

- Crush Revolving Balances First: Credit cards impact your DTI through their minimum monthly payments. Target the cards with the highest minimum payments first to wipe out those heavy monthly obligations quickly.

- Freeze All New Borrowing: Do not finance a car, purchase furniture on credit, or open new store cards within 6 to 12 months of a major loan application. New accounts add fresh monthly payments that can ruin your ratios.

- Boost Documented Income: Earning more money automatically dilutes your debt ratio. Freelance gigs, consistent overtime, or side businesses work beautifully, provided you can show a stable, verifiable track record.

- Eradicate Small Installment Loans: If you have an auto loan or a personal loan with just a few payments left, pay it off completely. Eliminating that full monthly payment instantly clears space in your budget.

- Consolidate High-Interest Debt: Merging multiple volatile credit card bills into a single, lower-payment consolidation loan can significantly reduce your total monthly liabilities.

- Release Co-Signed Liabilities: If you co-signed a loan for a friend or relative, lenders count that entire payment against you. If that person can refinance the loan entirely in their own name, that liability vanishes from your calculations.

A Tale of Two Borrowers: The True Cost of High DTI

Let us look at a real-world scenario to see how this plays out in dollars and cents. Meet two buyers with identical incomes and identical credit scores.

- Borrower A: Gross income of $6,000, monthly debts of $1,560. Back-end DTI is 26%. Result: Smooth conventional approval with the absolute lowest market interest rates.

- Borrower B: Gross income of $6,000, monthly debts of $2,520. Back-end DTI is 42%. Result: Limited to an FHA loan with a significantly higher interest rate.

The only difference between them was an extra $960 in monthly debt obligations. That seemingly small gap will cost Borrower B well over $20,000 in unnecessary interest payments over the lifespan of a 30-year mortgage.

5 Critical DTI Blunders That Stop Loans in Their Tracks

- Financing a Vehicle Right Before Applying: Adding a heavy car payment right before underwriting can instantly destroy your borrowing capacity for a home.

- Ignoring DTI and Only Monitoring Your Credit Score: A flawless 800 credit score cannot save an application if your debt load is completely maxed out.

- Forgetting About Co-Signed Agreements: Underwriters look at everything. Even if you do not pay a cent toward a co-signed loan, the full payment is legally factored into your DTI.

- Miscalculating Deferred Student Loans: Leaving deferred student loans out of your math is a huge mistake. FHA guidelines require underwriters to estimate 0.5% to 1% of the total balance as a monthly payment anyway.

- Using Net Income for Your Calculations: Running your personal math using take-home pay makes your DTI look much worse than it actually is. Always use pre-tax gross income to stay aligned with standard underwriting practices.

Frequently Asked Questions (FAQs)

What is a good debt-to-income ratio for a loan?

A ratio of 36% or lower is widely considered good by traditional mortgage and personal lenders. Staying under 28% is ideal and positions you to secure premium interest rates. Ratios between 36% and 43% are acceptable, but you may face stricter scrutiny.

How do I calculate my debt-to-income ratio?

Add up all of your mandatory monthly debt payments, divide that number by your pre-tax gross monthly income, and multiply the result by 100. Do not include standard living costs like utilities or insurance in this calculation.

What is the difference between front-end and back-end DTI?

Front-end DTI only measures your future housing costs against your monthly gross income. Back-end DTI calculates your housing costs combined with all other recurring debts, like credit cards and auto loans. Lenders place the heaviest weight on back-end DTI.

Does my debt-to-income ratio affect my credit score?

No, it does not directly affect your score because your income and DTI do not appear on credit reports. However, paying down the credit card debt required to lower your DTI will naturally reduce your credit utilization, which causes your credit score to rise.