Most people expect a wall of confusing financial jargon when looking into retirement accounts. What you actually need is a simple, straightforward explanation—the kind a financially savvy friend would give you over coffee.

The cash decisions you make early in your career carry way more weight than choices made down the road. In the world of investing, time is your ultimate superpower. Let us break down the choices clearly, honestly, and entirely free of finance-bro chatter.

The Big Two: 401(k) and Roth IRA Explained

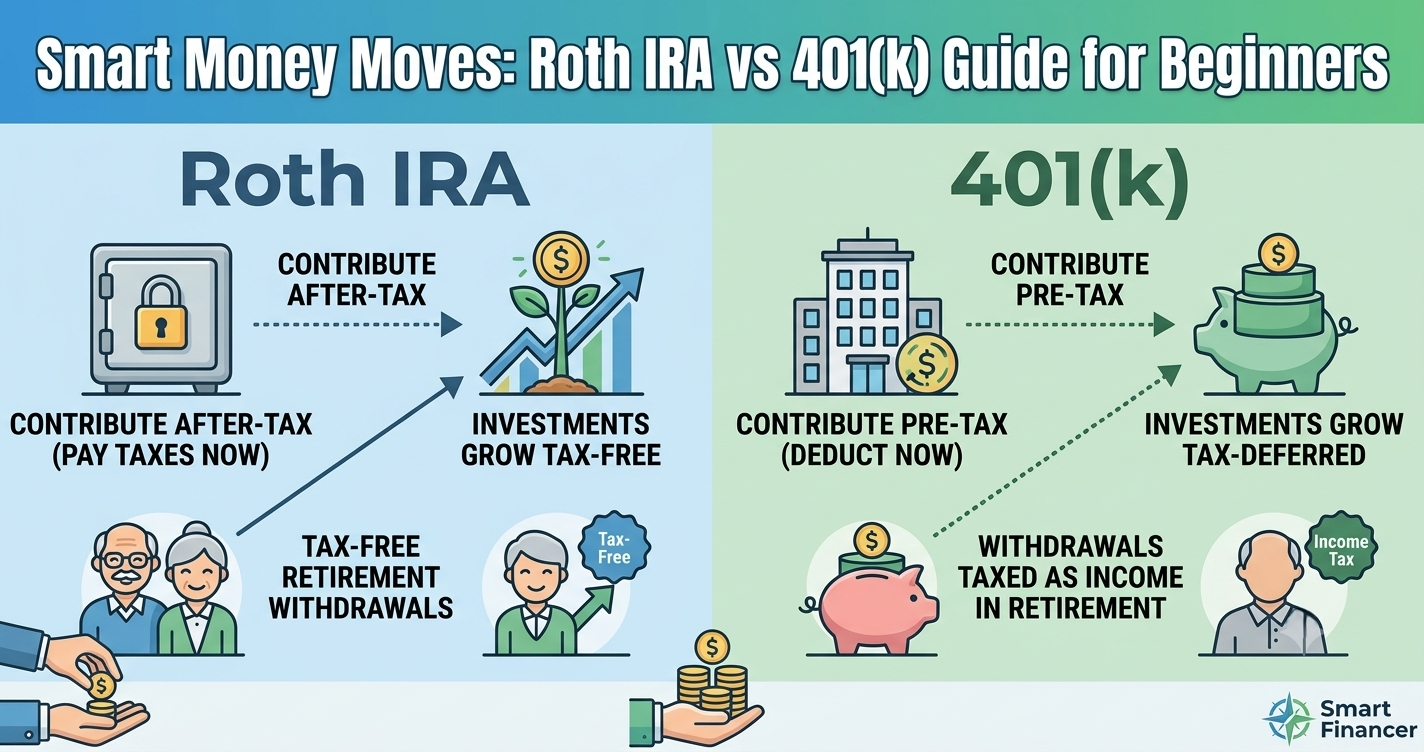

A 401(k) is a retirement plan set up directly through your job. Every single pay cycle, a percentage of your salary goes straight into your fund before the cash ever lands in your checking account. It automates your savings habit while lowering your taxable income for the year. Even better, many companies drop extra money into your account just for participating.

A Roth IRA is an account you open completely on your own through an online brokerage platform. You fund it using money that has already been taxed. Because you pay Uncle Sam upfront, the trade-off is massive: every single penny you withdraw during retirement is 100% tax-free. For a young adult, that means decades of pure, untaxed compound growth.

Side-by-Side Comparison: Rules and Limits

The IRS adjusted the rules for retirement accounts, making it a great time to map out your investment strategy. The table below details exactly how these two accounts stack up.

| Feature | 401(k) Plan | Roth IRA |

| Account Setup | Provided by your employer | Opened independently by you |

| Tax Break Timing | Immediate (lowers today’s taxes) | Future (tax-free withdrawals later) |

| 2026 Contribution Limit | $24,500 (under age 50) | $7,500 (under age 50) |

| Catch-Up Limit (Ages 50–59) | $32,500 total | $8,600 total |

| Employer Match Opportunity | Yes, very common | No, self-funded only |

| Income Restrictions | None | Yes (limits for high earners) |

| Early Withdrawal Rule | 10% penalty before age 59½ | Original contributions come out anytime |

How to Build the Ultimate Savings Strategy

If you are stuck choosing between the two, stop overthinking. The smartest move for beginners is to use both accounts together using a simple three-step sequence.

First, contribute just enough to your workplace 401(k) to grab every single dollar of your employer’s match. Missing out on a match is essentially turning down a portion of your salary. Second, open up a Roth IRA and focus on maxing it out to secure that sweet tax-free growth. Finally, if you still have cash left over that you want to invest, go back to your workplace 401(k) and bump up your percentage. This playbook gives you the perfect mix of free company money and future tax protections.

Frequently Asked Questions (FAQs)

What is the absolute main difference between a 401(k) and a Roth IRA?

The main difference comes down to tax timing and account ownership. Your employer sponsors a 401(k) and uses pre-tax money, meaning you get a tax break now but pay taxes on withdrawals later. You open a Roth IRA yourself using after-tax money, making your retirement withdrawals entirely tax-free.

Are there salary limits for opening a Roth IRA?

Yes, the IRS limits direct contributions for high earners. For single filers, the ability to contribute fully phases out between $153,000 and $168,000 in income. If you earn more than that, you can still look into a legal strategy called a Backdoor Roth IRA.

Can I pull money out of these accounts if I face an emergency?

If you pull money from a standard 401(k) before age 59½, you will face income taxes and a harsh 10% penalty. A Roth IRA is much friendlier because you can withdraw your original cash contributions at any time without fees or penalties, though you must leave the investment earnings untouched.

Does my employer’s 401(k) match count toward my annual contribution limit?

No, it does not. The personal limit is strictly for the money coming out of your own paycheck. Any extra cash your company drops into your fund is pure bonus money on top of your personal cap, giving your balance an extra hidden boost.